Where the Uranium bottlenecks actually are

Capacity Factor — Post 1 of 6 in a series on US nuclear fuel cycle equities.

Energy is the critical bottleneck for AI infrastructure today. In The Half-Life of a Press Release, we examined recent Small Modular Reactor hyperscaler announcements and their critical dependence on nuclear fuel enrichment. In this piece, we will focus on American companies operating in this field.

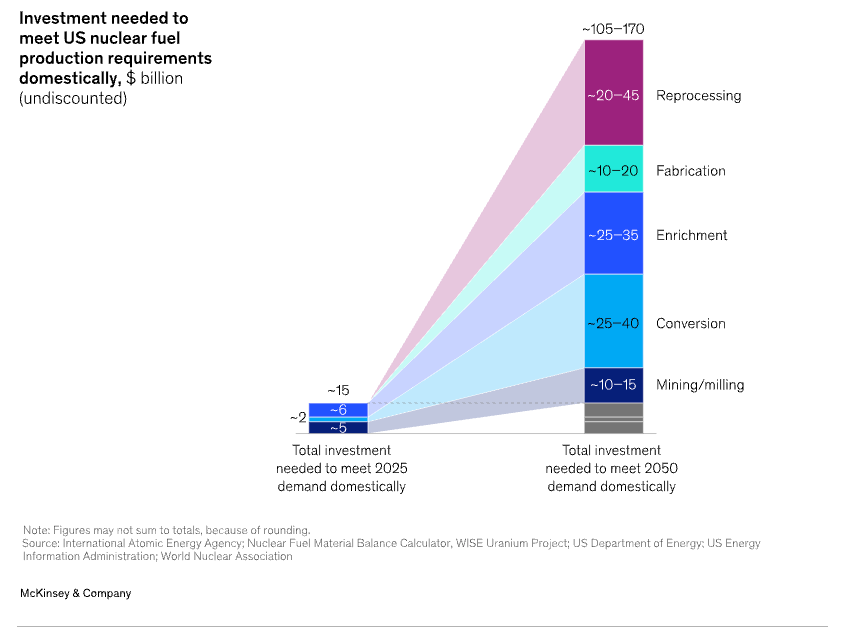

In May 2026, McKinsey published this report [1] on the US domestic nuclear fuel cycle that put a number on the rebuild: $105–170 billion of capex through 2050, split across mining, conversion, enrichment, fabrication, and reprocessing.

That’s a useful frame, but it’s not the investable number. The investable number is which one or two segments will absorb more than half of the new awards in the next 36 months, because the rest of the chain cannot move without them.

This is the first in a six-part series on US-listed nuclear-fuel-cycle equities. I screened 22 names against four filters — small/mid-cap, off all-time-high, accelerating fundamentals, and early narrative — and by the end of the series, I’ll be down to a five-name long book.

But before any of that, you have to understand where the bottlenecks actually are. They are not where most of the public conversation says they are.

The five segments and what they cost

The fuel cycle decomposes into five sequential nodes plus two adjacencies (reactors and waste/storage). Here’s the McKinsey capex stack:

If you read those numbers naively, reprocessing is the biggest opportunity. It isn’t. Commercial reprocessing has been effectively blocked in the US since Jimmy Carter’s 1977 executive order [2] and remains uninvestable on any horizon shorter than a decade. The capex range is wide because it’s a greenfield-risk number for a thing that probably won’t get built before 2040.

Mining looks underweighted at $15–20B. It is but globally, there is no shortage of uranium-producing capacity. Kazatomprom alone supplies roughly 40% of global production at low cost [3]. Adding US mining is a national-security argument, not a global-capacity argument. The investable angle in mining is uranium-spot beta plus US-specific permitting and ramp execution — not ground-up mine economics.

The interesting numbers are conversion and enrichment.

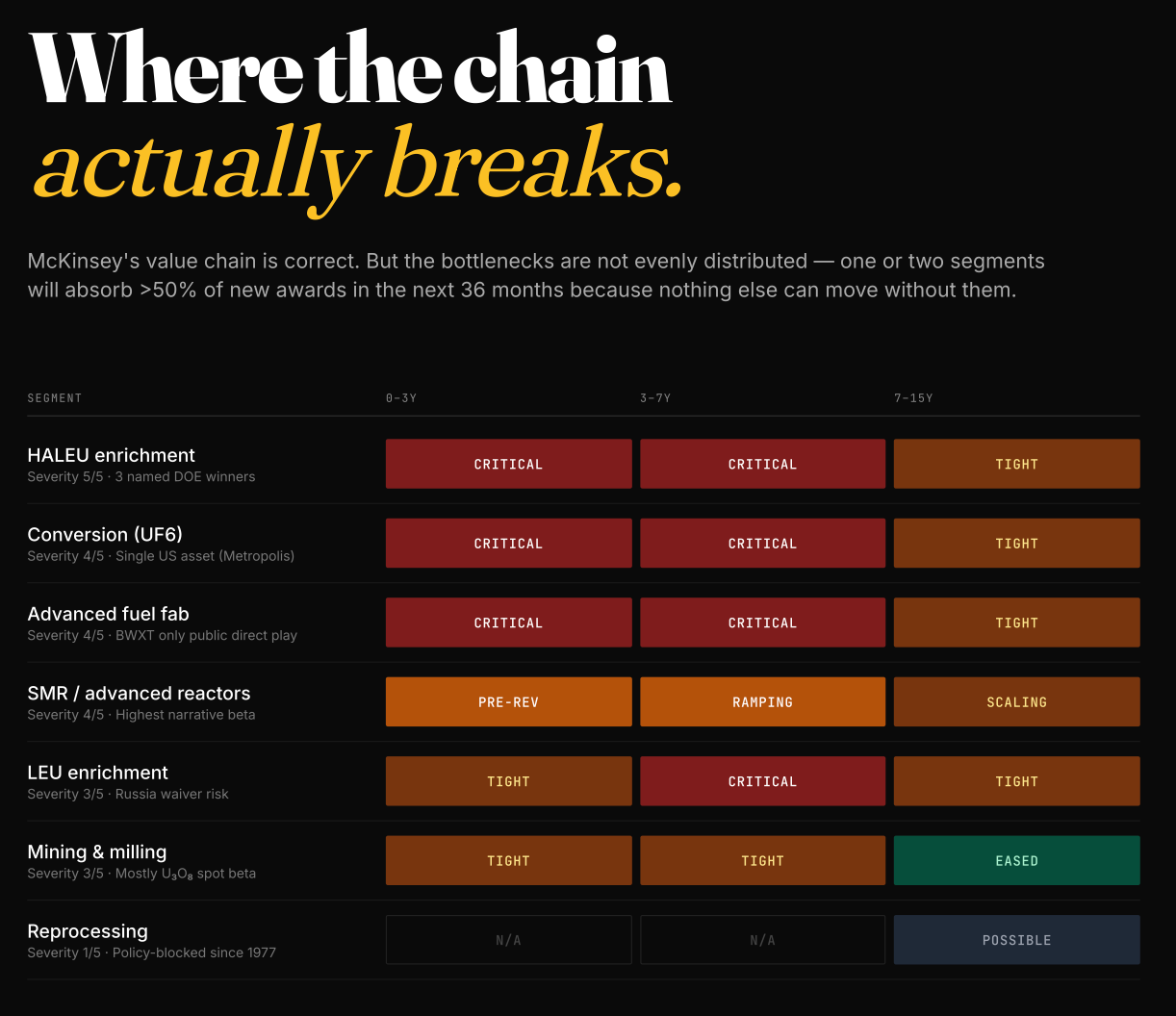

Where the bottleneck actually is

I’d score the seven nodes like this for severity over the next decade. Severity scale: 5 = single point of failure for the chain; 1 = not a binding constraint.

Three observations from this table that surprised me when I started doing this work.

First, HALEU enrichment is the single tightest knot in the chain.

HALEU — high-assay low-enriched uranium, 5–19.75% U-235 — is what every advanced reactor needs for its first core:

Oklo Aurora,

TerraPower Natrium,

X-energy Xe-100,

Kairos Power KP-FHR.

Until 2024, virtually all commercial HALEU came from Russia. Today, Centrus Energy has produced the first ~900 kg of US-origin HALEU at Piketon, Ohio. That is the entire commercial Western supply.

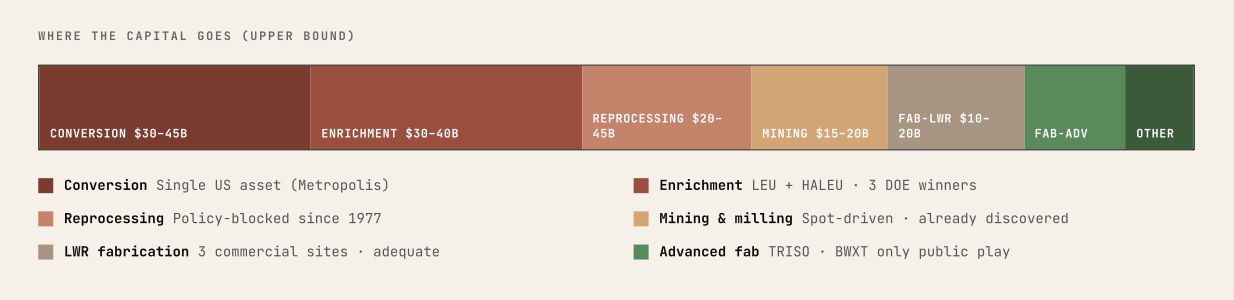

Second, conversion is almost as tight — and there is no way to play it directly on the listed US tape.

The single operating US conversion facility is ConverDyn’s Metropolis Works in Illinois, running at roughly 7 ktU/yr against an original nameplate of 15 ktU/yr. Its parent is Honeywell. Honeywell is a $137B mega-cap where conversion is a low single-digit percent of revenue. There is no listed pure-play. This matters for the screen because it means even if you correctly identify conversion as the tightest commercial bottleneck, you cannot express it cleanly through a single name. Anyone who tells you they have a “conversion trade” via Honeywell is overstating their position.

Third, advanced fuel fabrication (TRISO and metallic alloys) is also acute, with similarly thin investable exposure. The NRC granted X-energy the first-ever Category II TRISO fuel fabrication license in February 2026. X-energy is private. The only public direct play in advanced fuel fab is BWX Technologies (NYSE: BWXT) — and BWXT is a $19B mid-cap trading near its all-time high, well-covered, and structurally above the size cap most thematic books carry.

Mining sits below those three in severity. It is a thematic-beta trade with a structural overlay, not a structural trade with a price overlay. That distinction matters: if uranium spot rolls over 25%, mining-name multiples compress fast. The conversion and HALEU bottlenecks don’t decompress that way.

The DOE award everyone should be paying attention to

On January 6, 2026, the US Department of Energy awarded $2.7 billion [4], split evenly three ways:

$900M to American Centrifuge Operating (a Centrus Energy subsidiary) for HALEU at Piketon, Ohio.

$900M to General Matter for HALEU at the former Paducah Gaseous Diffusion Plant in Kentucky. General Matter only emerged from stealth in April 2025 and signed its DOE land lease in August 2025.

$900M to Orano Federal Services for LEU at Project IKE in Oak Ridge, Tennessee — a piece of a roughly $5B greenfield enrichment project.

Plus a smaller $28M supplemental award to Global Laser Enrichment [5] (Silex / Cameco JV) for next-gen technology.

The structure of this award is, to me, the most consequential signal in the McKinsey article. The federal government had a choice: concentrate the bet behind one US-owned producer, or seed three separate efforts. It chose three. That decision compresses per-name optionality versus a winner-take-all outcome, but it converts the question from “will US-owned HALEU exist?” (speculative) to “which of three named producers will execute first?” (handicapping).

Two of the three are private. The only listed name that won a tranche is Centrus Energy (NYSE: LEU). That is why every conversation about US enrichment exposure starts and often ends with Centrus — the math of public-market exposure forces it.

What this means for stock-picking

If you’re a thematic investor with a US-listed mandate, the McKinsey frame collapses to a few hard observations.

1. HALEU enrichment is where bottleneck severity, federal funding, and listed exposure all converge. This is where the work has to be most rigorous, because the names are crowded and the cone of outcomes is wide.

2. Conversion is structurally critical but offers no clean public expression. A future Solstice / Honeywell Advanced Materials spinoff is the most-watched corporate-action catalyst in the cycle.

3. Mining is investable but it is a uranium-price trade with a structural overlay, not the other way around. The order of those words is the difference between a 30% drawdown and a five-bagger.

4. The picks-and-shovels lane — waste handling, dosimetry, decommissioning instrumentation — is its own structural thesis, and there is exactly one filter-compliant mid-cap in it. I’ll come back to that in Post 4.

5. The advanced reactor adjacency (NuScale, Oklo, Nano Nuclear, BWXT, GE Vernova) is the demand engine for the entire chain. But FOAK economics are still unproven and the narrative is loud. Post 5.

The single most important question I’m asking through the rest of this series isn’t “which of these names is great.” It’s “which of these names is great at a price I should actually pay.” Most of them aren’t, today.

What’s coming

Post 2 — HALEU enrichment. Centrus Energy as the McKinsey anchor name. ASP Isotopes’ Quantum Leap Energy subsidiary as the optionality slot. Why I think one of these is fundamentally cheap right now and the other one isn’t.

Post 3 — Conversion. The bottleneck nobody can play directly, and the Solstice spin that might fix that.

Post 4 — Picks-and-shovels. One mid-cap that passes the screen in two of seven segments simultaneously.

Post 5 — SMR demand. Why I think the post-CFPP-cancellation reset on NuScale is more advanced than the market recognizes — and why that doesn’t mean I’m long.

Post 6 — The book. Five-name long book, position-sized, with explicit falsification triggers for each.

Subscribe if you want this in your inbox over the next few weeks.

Further reading

[1] McKinsey & Co. — Understanding domestic nuclear fuel production options in the United States

[2] Jimmy Carter’s Executive Order

[3] Kazatomprom - Uranium market

[4] DOE — Awards $2.7 billion to restore American uranium enrichment

[5] ANS Nuclear Newswire — DOE awards $2.7B for HALEU and LEU enrichment

World Nuclear News — US enrichment funding recipients flesh out plans

Prohibiting Russian Uranium Imports Act P.L. 118-62

*Capacity Factor is a six-part series on US nuclear fuel-cycle equities. Next post: HALEU enrichment.*