Where the HALEU bet actually pays

Capacity Factor — Post 2 of 6 in a series on US nuclear fuel cycle equities.

In Post 1, I argued that the tightest knot in the US nuclear fuel cycle is HALEU enrichment — high-assay low-enriched uranium, the 5–19.75% U-235 fuel that every advanced reactor in the US needs for its first core. There is no commercial Western HALEU supply at scale. Until 2024, it all came from Russia.

There are exactly two US-listed names with direct HALEU exposure. One of them is the obvious pick — funded by the Department of Energy, owned by ~80% of institutions, up 200% in the last twelve months. The other is a $700M micro-cap whose enrichment subsidiary you’ve probably never heard of.

Thanks for reading! Subscribe for free to receive new posts and support my work.

I think the smaller one is the better trade today. Not because the bigger name is bad, it isn’t, but because the market has already priced its bull case, and the smaller name is the only fundamentally cheap HALEU option in the US public market.

Here’s the work.

The two listed names

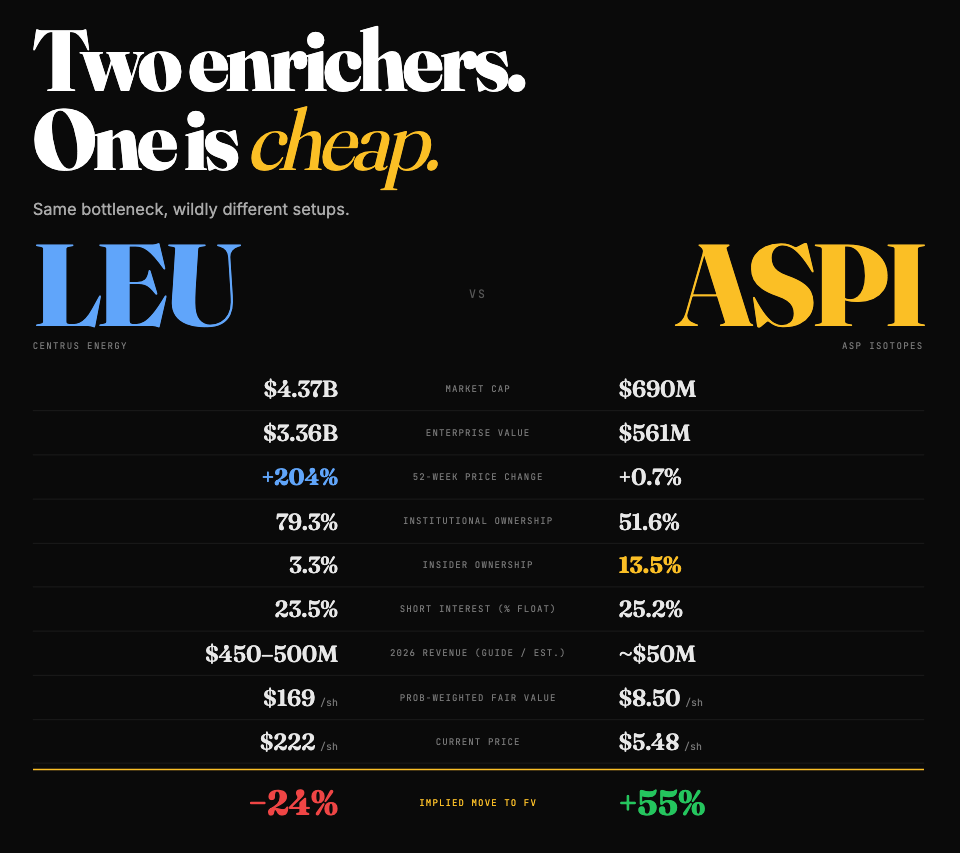

Centrus Energy (NYSE: LEU) is the name. It is the only US-owned commercial enricher and one of three companies funded by the DOE’s January 2026 $2.7B HALEU and LEU enrichment award.

Centrus’s American Centrifuge Operating subsidiary received $900M for HALEU production at Piketon, Ohio, and produced the first ~900 kg of US-origin HALEU. Centrus raised 2026 revenue guidance to $450–500M in its Q1-26 print (https://www.prnewswire.com/news-releases/centrus-reports-first-quarter-2026-results-302763250.html), and is sitting on a $3.9B contracted backlog. Market cap $4.37B.

ASP Isotopes (NASDAQ: ASPI) is the optionality name. Its core business is laser-based isotope enrichment for medical (Mo-99 path), semiconductor (Silicon-28), and pharmaceutical applications. The HALEU exposure is via a wholly-owned subsidiary, Quantum Leap Energy (QLE), which holds a long-term HALEU offtake agreement with TerraPower plus a $22M conditional loan, and which signed a non-binding MOU in March 2026 (https://www.stocktitan.net/news/ASPI/) with a major US nuclear power operator for HALEU, LEU+, uranium conversion, and deconversion services. Market cap $690M, of which $333M is cash as of December 2025.

The numbers side-by-side:

If you only look at the top three rows, Centrus is obviously the better company. It has revenue, it has guidance, it has DOE money, and the chart has only gone up. ASP Isotopes is small, loss-making, and the stock has gone nowhere for a year while the rest of the nuclear thematic has rallied.

But the bottom three rows are where the trade actually lives.

Where the value actually is

I built probability-weighted scenario DCFs on both names.

Centrus scenarios (my P-weights):

Probability-weighted fair value: ~$169/share. Current price $222. That gap doesn’t mean Centrus is overvalued in any absolute sense — it means the market is pricing the bull-case outcome at roughly 60–70% probability, versus my 30%. Either I’m wrong about the probabilities, or the market is paying ahead of execution. Both can be true at once.

ASP Isotopes scenarios:

Weighted operating NPV ~$0.74B, plus $333M cash on hand → fair equity ~$1.07B. Current market cap $690M. That’s a +55% asymmetric setup, with the cash backstop providing a soft floor.

Three observations from running these numbers.

First, the asymmetry runs in opposite directions. Centrus’s bear case is –80% from current; ASPI’s bear case is –78%. That looks similar. But ASPI’s bear case still leaves you with $150M of NPV against $333M of cash, so the actual equity floor is higher than the bear-NPV number suggests. Centrus’s bear case has no cash floor — it’s a working business, and the bear case is operational impairment. The shape of the downside is different even when the magnitude is similar.

Second, insider ownership is doing real work. ASPI’s 13.5% insider ownership versus Centrus’s 3.3% (and NuScale’s 0.4%) is the kind of management-alignment signal that tends to matter at exactly the inflection moment ASPI is approaching — the 2026 commercial-shipment year. Founders who own the company tend not to price-collapse it on the first dilutive raise.

Third, the TerraPower offtake is a third-party validation that the market hasn’t internalized. TerraPower is privately held, well-funded, and has every incentive to source HALEU from the most credible producer it can find — including, in theory, from Centrus directly. The fact that TerraPower committed offtake terms and a $22M conditional loan to QLE specifically tells you the market is too pessimistic on QLE’s technical credibility.

The catalysts most people aren’t tracking

Both names have a thick catalyst calendar through the end of 2027. The two that matter most for getting positioning right are very specific.

For Centrus, the binary is the Q2-26 print in August, where management will disclose Piketon HALEU production cadence in kg/month run-rate. The current implied schedule has Piketon ramping toward roughly 6 metric tons per year of HALEU output by 2028. That implies a run-rate around 80 kg/month at maturity. If the August print shows the production cadence tracking below ~40 kg/month — half the implied path — the bear case activates fast and the multiple compresses with it. If it tracks at or above 60 kg/month, the bull case stays alive, and the stock probably runs further before consolidating.

For ASPI, the binary is QLE’s first HALEU pilot output disclosure, expected in Q4 2026. This is the cleanest existence proof the market has been waiting for. If QLE produces enriched material on schedule, the bull-case probability re-weights upward — and at a $690M market cap, the re-rating math is significant. If QLE misses by more than two quarters, the bear-case probability dominates, and the cash floor becomes the only thing holding the stock up.

Two other dates worth flagging:

The Russia uranium waiver expiry in 2027 — under the Prohibiting Russian Uranium Imports Act is a structurally positive catalyst for both names, but more so for Centrus, which loses Russia LEU revenue but gains tighter pricing on its US-domestic enrichment.

Centrus’s first commercial HALEU shipments, targeted for Q2 2027, are the bull-case proof point. If those land on schedule with TerraPower, X-energy, or Kairos as the first counterparty, Centrus becomes harder to fade.

What this means for stock-picking

1. Centrus is the right structural answer to the wrong question. “Which name has the most HALEU exposure?” gets you to LEU. “Which HALEU name offers asymmetric upside at current prices?” gets you to ASPI. Both questions are valid, but only one is a trade.

2. The size discount is doing the lifting. ASPI is small enough that institutional ownership hasn’t yet crowded out the asymmetry — 51.6% versus Centrus’s 79.3%. The same business at $4B of market cap would already be priced in line with Centrus.

3. Optionality positions need explicit exits. I would hard exit if QLE produces no enriched HALEU material by year-end 2026, or if TerraPower offtake terms are publicly restructured downward. The cash backstop makes the position survivable; the falsification triggers make it disciplined.

4. Centrus is a buy on pullback, not a buy on chase. I would build a position below $165, where the implied bull-case probability falls into a range that matches my analytical view. Above $200, the math doesn’t work even on aggressive assumptions.

5. Both names will be revisited together every quarter. The catalyst structure is interlocking — Centrus’s Piketon cadence and ASPI’s QLE pilot are the two existence proofs that determine whether US-owned HALEU is real or theoretical. Watching only one of them gives you half the signal.

What’s coming

Post 3 — Conversion: the bottleneck nobody can play directly. Why ConverDyn / Solstice’s Metropolis Works is the single tightest commercial chokepoint in the chain, and how an HON Advanced Materials spin (rumored, not confirmed) would unlock the cleanest pure-play if it ever lists.

Post 4 — *Picks-and-shovels*. The mid-cap that passes the 4-variable filter in two of seven segments simultaneously, and why I think it’s a satellite rather than a core position, despite that.

Post 5 — *SMR demand*. Why I think the post-CFPP-cancellation reset on NuScale is more advanced than the market recognizes — and why that doesn’t yet mean I’m long.

Post 6 — *The book*. Five names, position-sized, with explicit falsification triggers for each.

Subscribe if you want this in your inbox over the next weeks.

Further reading

- DOE — *[Awards $2.7B to restore American uranium enrichment](https://www.energy.gov/articles/us-department-energy-awards-27-billion-restore-american-uranium-enrichment)* (Jan 6, 2026)

- Centrus Energy — *[Q1-26 results press release](https://www.prnewswire.com/news-releases/centrus-reports-first-quarter-2026-results-302763250.html)*

- ASP Isotopes — *[Q3-25 10-Q via SEC EDGAR / StockTitan summary](https://www.stocktitan.net/sec-filings/ASPI/10-q-asp-isotopes-inc-quarterly-earnings-report-b8eb89c3dea3.html)*

- World Nuclear News — *[US enrichment funding recipients flesh out plans](https://www.world-nuclear-news.org/articles/us-enrichment-funding-reactions)*

- ANS Nuclear Newswire — *[DOE awards $2.7B for HALEU and LEU enrichment](https://www.ans.org/news/article-7652/doe-awards-27b-for-haleu-and-leu-enrichment/)*

- Prohibiting Russian Uranium Imports Act ([P.L. 118-62](https://www.congress.gov/bill/118th-congress-house-bill/1042), May 2024)

---

*Capacity Factor is a six-part series on US nuclear fuel-cycle equities.

Thanks for reading! Subscribe for free to receive new posts and support my work.